R&D Summary Report

R&D (Research and Development) summary report is the part where businesses officially declare the income tax withholding incentive they benefit from on the wages of personnel working in R&D, innovation or design activities within the scope of Law No. 5746. This report is prepared to show that the incentive has been calculated and applied correctly and to notify the tax office. Income Tax Withholding Incentive within the Scope of Law No. 5746 ensures that the income tax calculated on the wages earned by R&D, design and support personnel for the time they actually work on these projects is reduced (abandoned) at certain rates.

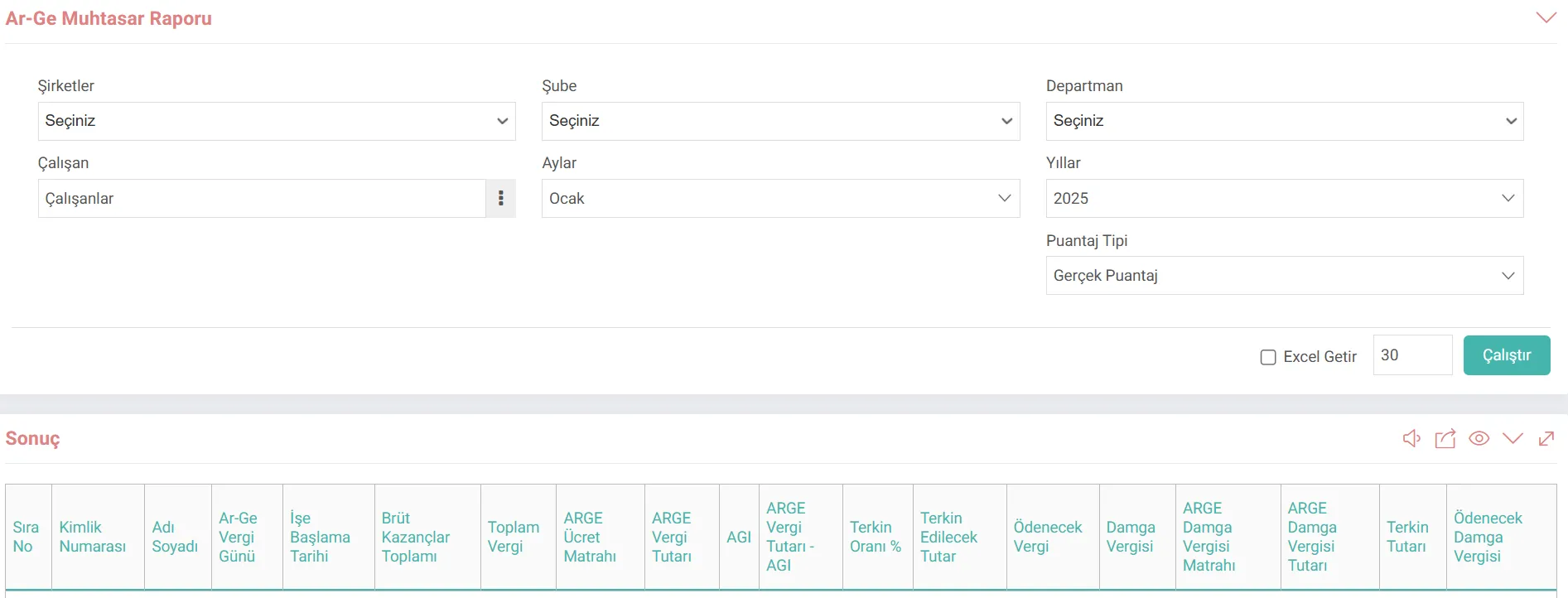

Path: BI-Report > Standard Reports > HR - HR Reports > Wage Management and Personnel

Incentive Rates

Although incentive rates vary depending on the education level of the personnel and the region where they are located, the most commonly used rates are based on education level. These rates are applied based on the wage portion corresponding to the time the personnel actually works in the R&D or design center. For example; if a staff member spends 80% of his time in R&D, 80% of his wage benefits from the incentive.

How the Incentive is Implemented

- Wage Calculation: Normal income tax on the gross wage of the staff. is calculated.

- Incentive Calculation: The part of the calculated income tax corresponding to the above rates (for example, 95%) is determined as incentive.

- Cancellation and Payment: The determined incentive amount is deducted (cancelled) from the income tax payable to the tax office. The employer does not pay this part to the state, but continues to pay the insurance premium in full on behalf of the personnel.

- Declaration: These canceled amounts are declared in detail in the R&D annexes of the Withholding and Premium Service Declaration (MUHSGK).

The R&D Withheld report is received on a month/year basis and by selecting Real Score in the tally type field. Report criteria can be narrowed depending on company, branch, department and employee selection. Optionally, reports can be obtained only on a branch basis or on a single employee basis.

- R&D Tax Day: The number of days that the personnel actually worked in R&D or design activities that month, e.g. 30 days if the employee worked 30 days in R&D in a 30-day month.

- Starting Date: The date the personnel started working.

- Total Gross Earnings:The total gross wage of the personnel for that month.

- Total Tax:Gross wage "SGK worker The monthly total income tax amount found as a result of the tax tariff applied to the remaining income tax base after deducting the "share" and "unemployment premium".

- R&D Wage Base: The part of the wage that falls within the scope of R&D according to the ratio of days/duration worked by the personnel in R&D. For example; Total Wage Base x (R&D Day / Total Working Day).

- R&D Tax Amount: Income tax amount corresponding to the R&D wage base. This amount is the main tax portion to which the incentive will be applied.

- AGI: 0 income for after 2022 or subtracted from the calculation

- R&D Tax Amount - AGI: R&D tax amount less any AGI (no more) if any. This determines the tax amount based on cancellation.

- Abandonment Rate %: Withholding tax reduction rate determined in Law No. 5746 according to the education and qualifications of the personnel For example; 95% for PhDs, 90% for others or 80%

- Amount to be Withheld: (R&D Tax Amount - AGI) amount.

- Stamp Duty: The total amount of stamp duty normally deducted from the gross wage.

- R&D Stamp Duty Base: The fee base within the scope of R&D on which stamp duty is calculated.

- R&D Stamp Duty Amount: R&D stamp duty base. stamp duty amount.

- Cancellation Amount: Within the scope of Law No. 5746, wage slips related to R&D activities are exempt from stamp duty. Therefore, this amount must be equal to the R&D stamp duty amount. (That is, the stamp duty on R&D is completely cancelled).

- Stamp Tax to be Paid: The remaining stamp tax to be paid by the employer after deducting the cancellation amount from the total stamp duty amount.

Sample Calculation

- Employee: Undergraduate R&D personnel.

- Period: November 2025.

- Total Working Days: 30 days (November).

- Abandonment Rate: 90%

- AGI: It will be accepted as 0 since it is removed in 2022.

- Income Tax Bracket: 15%

R&D Tax Day | 30 | Personnel in R&D all month (30 days) worked. |

Starting Business Date | 01.01.2024 | |

Gross Earnings Total | ₺30,000 | Monthly gross wage. |

Income Ver. Base | ₺25.000 | (Assumption: Gross Wage - SSI/Unemployment Worker's Share) |

Total Tax Base | ₺25.000 | (₺25.000 Base) x (30 R&D Days / 30 Total Days) = ₺25.000 |

R&D Tax Amount | ₺3.750 | R&D Base tax: |

AGI | ₺0 | Abolished as of 2022. |

R&D Tax Amount - AGI | ₺3.750 | |

Abandonment Rate % | 90% | The rate determined by law. |

To be Abandoned Amount | ₺3.375 | (This amount is covered by the Treasury.) |

To be paid Tax | ₺375 | ₺3.750 (Total Tax) - ₺3.375 (Cancellation) |

Stamp tax Base | ₺30,000 | Gross fee for R&D (accounted for the entire gross fee). |

R&D Stamp Tax Amount | ₺227.70 | Stamp Tax on R&D Base. |

Cancellation Amount | ₺227.70 | R&D personnel wages within the scope of Law No. 5746 are completely exempt from Stamp Tax (Deferral rate is 100%). |

To be paid stamp duty It shows that ₺3,375 of the ₺3,750 income tax and stamp duty deducted from the paid wage are fully covered by the Treasury (they do not come out of the employer's pocket). Amount | Amount to be Paid After Incentive | |

Income Tax Tax | ₺227.70 | ₺0 |