Securities

Securities buying, selling, dividend, valuation transactions can be done through the Securities module.

Market-Variable Securities Purchase and Increase / Decrease in Value Transactions

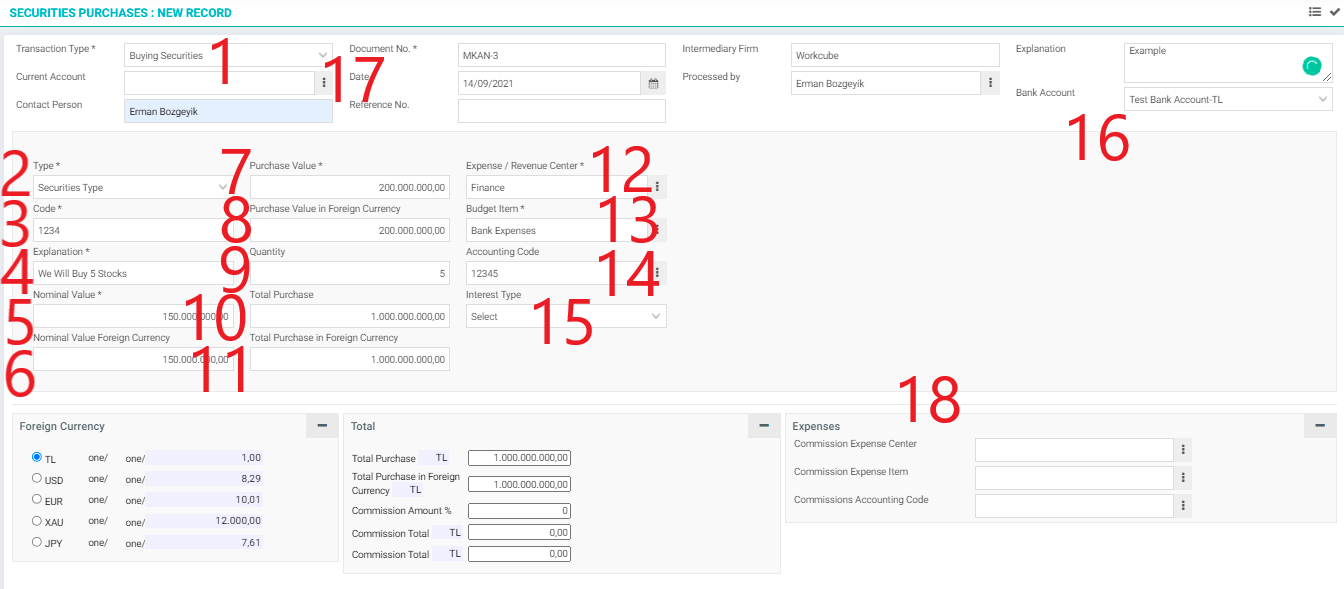

5 Stocks with a purchase value of 200,000 USD and a variable market value and dividend yield type will be purchased.

Below is the screen we will use for this process. To reach this screen, you must follow this route:

Route: ERP > Finance-Accounting > Securities > Securities Purchases

Warning: As stated in the pre-transactions, definitions must be made in order to purchase any securities.

Info Fields and Definitions

- Transaction Type: It is the definition that determines the current, accounting, and budget transaction rules and user authorizations.

- Securities Type: It is the parametric definition that groups the securities.

- Code: Securities, especially stocks, have unique transaction codes. Workcube makes collection, grouping, and reporting according to these codes.

- Explanation: Enter the explanation and notes for the transaction.

- Nominal Value: Securities may have increased in value or decreased in value, the face value indicates one value on the book.

- Nominal Value Foreign currency: The nominal value is written in foreign currency.

- Purchase Value: Displays the unit price of this security, regardless of its face value or current market value.

- Purchase Value in Foreign Currency: The foreign currency equivalent of the purchase value is written.

- Quantity: The amount received is written.

- Total Purchase: It is the purchase value and the diameter of the quantity.

- Total Purchase in Foreign Currency: The foreign currency equivalent of the total purchase amount is written.

- Expense / Revenue Center: Records which budget center makes the purchase of securities.

- Budget Item: Records under which budget item the purchase of securities will be followed.

- Accounting Code: Records under which accounting account the purchase of securities will be followed.

- Interest Type: A parameterized definition used to group and report returns such as dividends and rents.

- Bank Account: Records which bank account the security was purchased using. Bank transactions are made up to the purchase amount.

- Current Account: If an intermediary institution is used for the purchase of securities and the purchase is made by the intermediary institution, the Current Account is selected. When a current account is selected, the bank cannot be used. The receivable account of the intermediary institution is run up to the purchase amount.

- Expenses: If a commission is paid to the intermediary institution, the expense center, expense item, and accounting account of the commission are selected.

Accounting of the Securities Purchased

When the security purchase transaction is recorded, depending on the "Make Accounting Transaction" option in the Transaction type, it makes an integrated accounting record by issuing the Offset Receipt.

To review the accounting records, it is sufficient to click the accounting receipt icon.

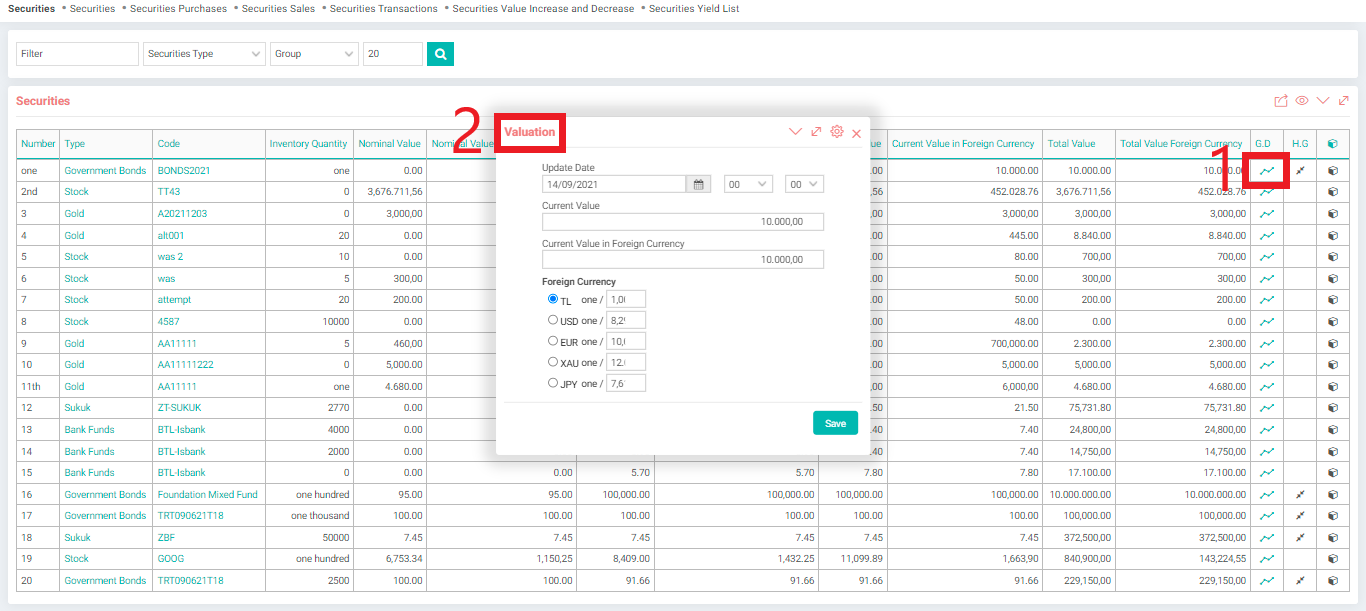

Securities History and Value Update

The values of the securities whose market value increases or decreases are updated whenever required. Value increase and decrease also make budget and accounting records. The securities list contains the last updated value information of the security. If desired, the current value of a security can be rearranged on the list.

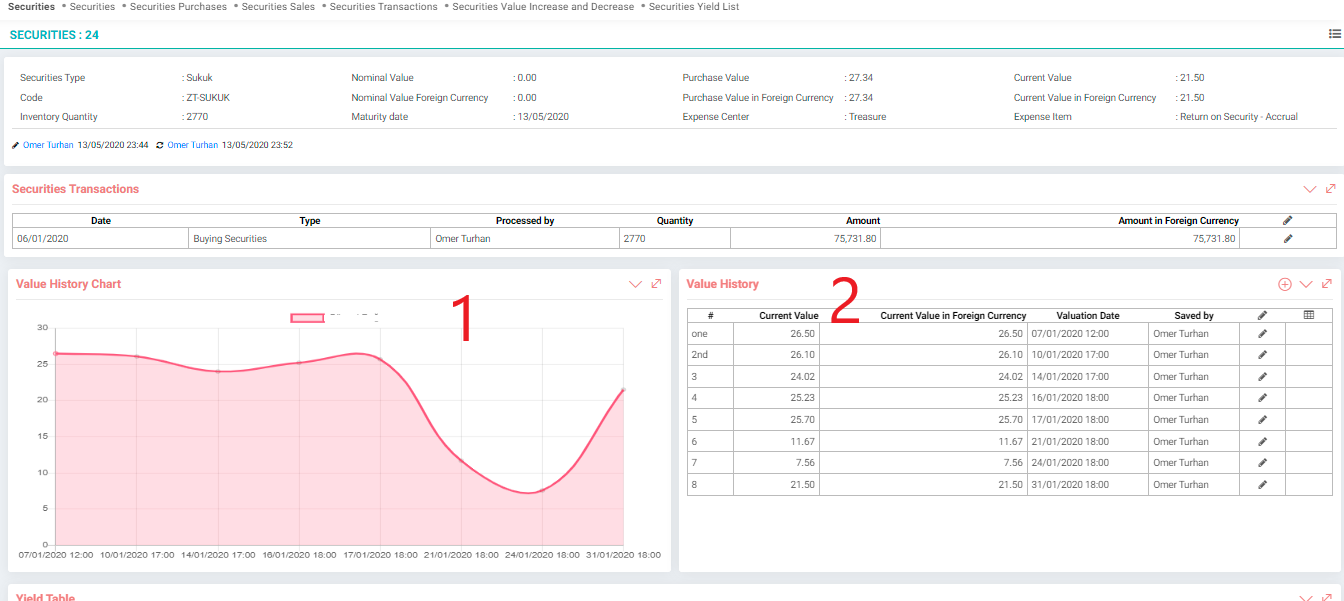

On the securities detail page, there is a table and graph of changes in value as well as relevant securities buying and selling information. In value update transactions, if the accounting and budget transaction options are set in the transaction category, the accounting and budget transactions are recorded. These records can be viewed from the relevant screens or from the trial balance and budget reports.

Suggestion:There is no obligation to record accounting and budget for each value update operation. At the end of the month or temporary tax periods, Value Increase and Decrease can be done collectively and accounting and budgeting can be done.

As can be seen in the example below, the graph changes as the value increases and decreases change.

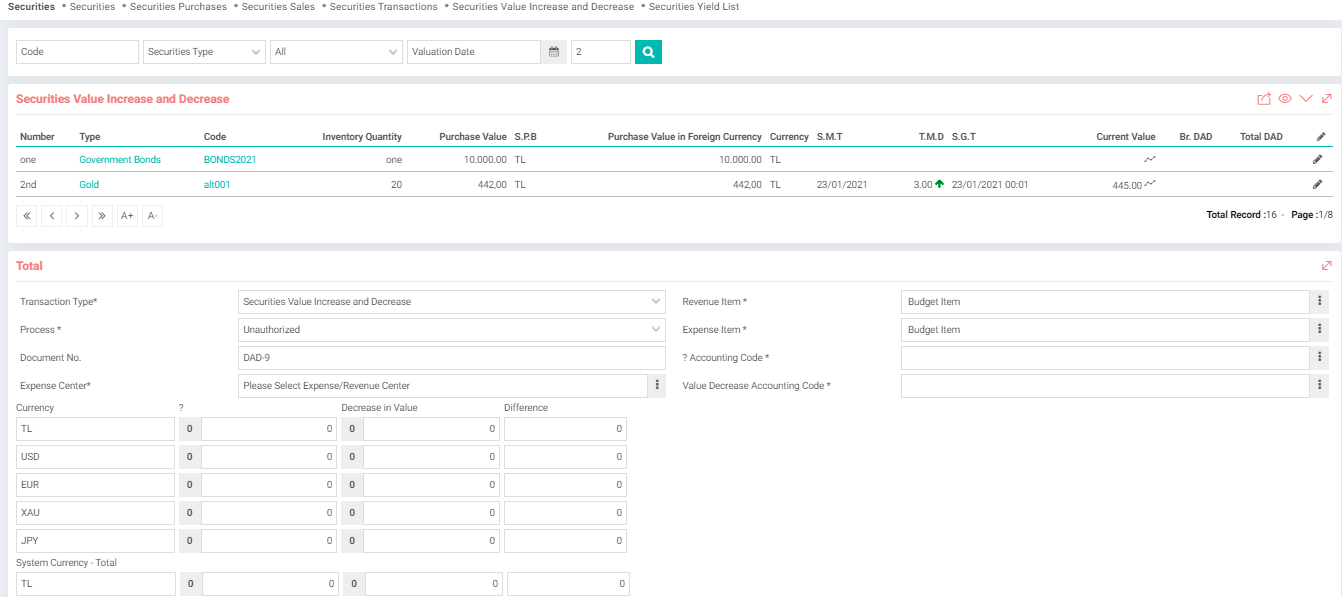

Multiple Securities Value Increase and Decrease Transactions

It is the screen where the recognition, income, and expense transactions of securities are made. In this list, the securities are filtered by selecting the date. If there is a decrease in its current value, its value is displayed in terms of unit and total amount. Securities for which value increase and decrease calculations are to be made are selected on a row basis. Each selected security is grouped according to its own trading currency and displayed in the total account. At the same time, the entire amount of increase and decrease is calculated with the currency in which the system works.

Warning: In the value increase and decrease process, the filter date directly affects the value increase and decrease account. It finds the increase and decreases between the last value before this date and the Last Valuation Date where accounting and budget transactions were made.

Info Fields and Definitions

- Transaction Type: It is the definition that determines the accounting and budget transaction rules and user authorizations.

- Process: It runs the workflow by defining the process-stages and authorities of the increase and decrease operation.

- Expense / Revenue Center: It determines in which budget center the increase and decrease in value will be recorded as profit and loss.

- Revenue Item: It determines which budget item the increase in value will be written as revenue.

- Expense Item: It determines which budget item the decrease in value will be written as expense.

- Value Increase Accounting Code: Records under which accounting account the value decrease will be followed.

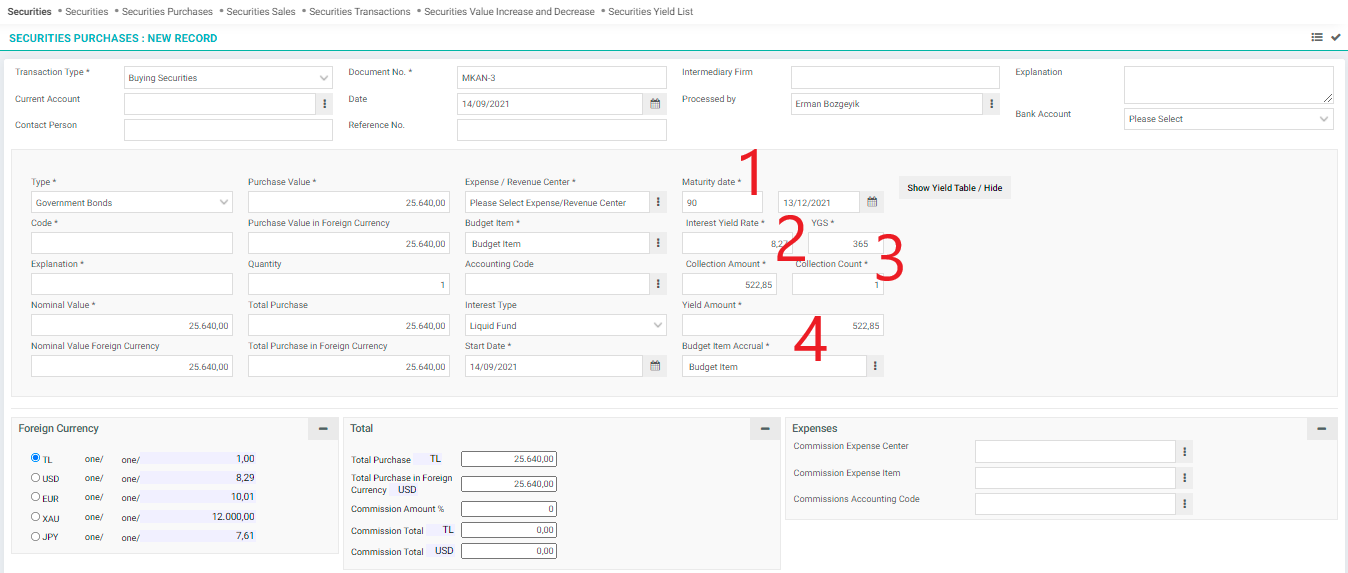

Fixed Income Securities Purchase and Income Transactions

In this example, a government bond with a purchase value of 25,640 USD and an annual interest rate of 8.90, and a maturity of 90 days will be purchased by selecting the yield type as Fixed income.

In fixed income securities, it automatically calculates the returns according to the total maturity of the return, the rate of return, the payment period-intervals of the return, and the number of collections and installments of the return.

In fixed income securities, it automatically calculates the returns according to the total maturity of the return, the rate of return, the payment period-intervals of the return, and the number of collections and installments of the return.

Additional Information Fields and Definitions in Fixed Income Securities Purchase Transaction

- Maturity: The total maturity-to-maturity of my security. For example, a 1-year government bond purchased on January 1, 2021 has a maturity of 365 days on December 31, 2021.

- Rate of Return: It is the annual rate of return in %.

- Yield Payment Period: In which interval or term the returns can be collected. For example, income is not paid once a month or until maturity.

- Number and Amount of Collection: Indicates how many installments and how much income can be collected in each installment.

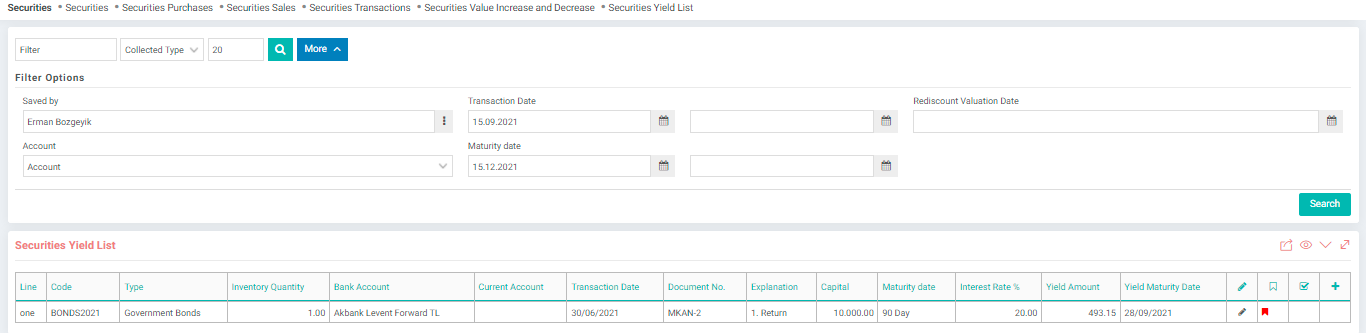

Securities Yield List

It lists the fixed income securities with different maturities such as coupons, dividends, and rents on a row basis. At the same time, the yields are transferred to the cash flow statement. Here are the answers to questions such as when and which returns should be collected from which securities and whether they were received. A useful list is provided to follow these processes.

Rediscount Transaction of Undue Securities Returns

If the return is requested to be valued at the end of the period before the maturity date of the return, the rediscount-discounting process is performed. On the screen above, a 16-day period-end valuation of fixed-income security with a maturity of 90 days has been made at the end of April, and accounting and budgeting have been done.

Warning: The point to be noted here is that the maturity dates on the yield lines and the rediscount date specified on the filter date above must be consistent. According to the selected rediscount date, the number of days over which the share will be entered into the income transaction is also indicated in the relevant line. On this screen, more than one securities can be valued at the same time, the boxes of the lines to be valued should be ticked. This box does not appear in the collected returns and the flag on the far right of the line appears as green.

Account Movement and Details of Fixed Income Securities

By clicking on the detail icon in the list of securities yields, the maturity of those securities, whether the returns are collected or not, and whether rediscount transactions are made, are displayed in detail.

Information Fields and Tables

- Yield Table: It is the table that shows the yield amounts according to the due dates and whether they are transferred to the account.

- Rediscount Table: It is the table that shows the dates on which the undue returns are transferred to the accounting tables by rediscounting.

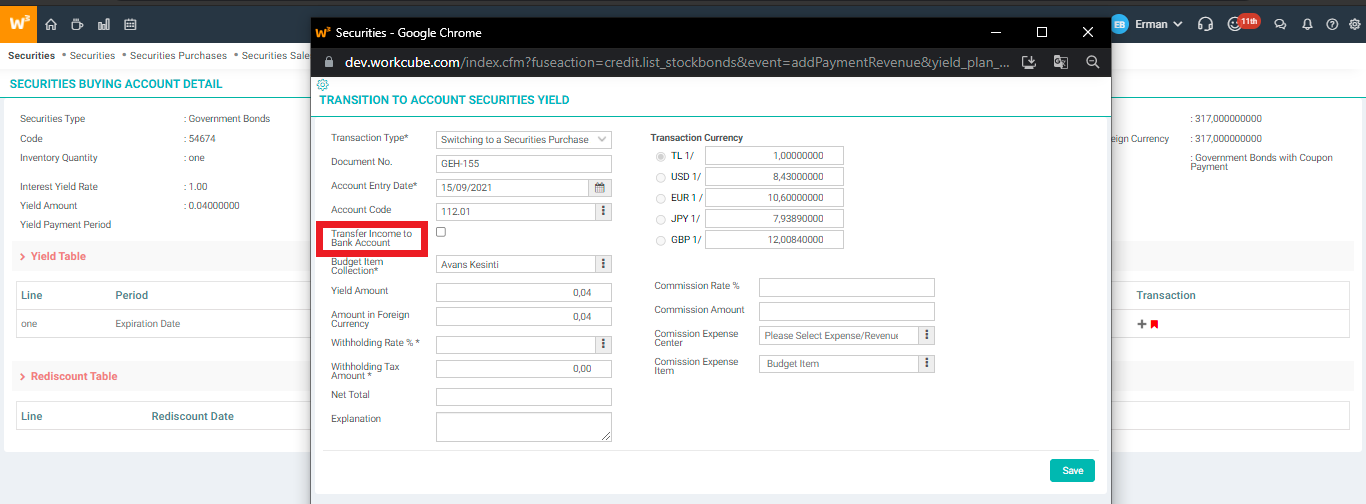

Tip: By clicking the + icon in the yield line, the account transition screen of the yield is opened.

Securities Return Account Transfer Transaction

In order to transfer the overdue returns to the bank account, the yield amount is transferred to the relevant bank account. For this transaction, a bank account is selected and a special transaction type such as money deposit and bank transfer is made.

Warning: Records should be made by taking into account whether the returns on the securities are subject to withholding or not. As it is known, there are taxes according to the types of securities determined by law. The bank or intermediary institution collects the withholding tax, which is followed in the prepaid taxes account, on behalf of the investor. In order for the withholding tax as prepaid tax to be followed according to the banks, the withholding rates must be defined according to the banks.

Accounting of Rediscounted Yields at Maturity

If the return has been rediscounted before, it is calculated by deducting the rediscount amount from the total return amount. Because accounting records have been made up to the amount of rediscount made previously. However, the difference should be subject to accounting treatment. The yield of the undue and rediscounted security is transferred to the bank account as a total-block at the end of maturity. When the rediscount bank does not make a transaction, it does not create a duplicate record.

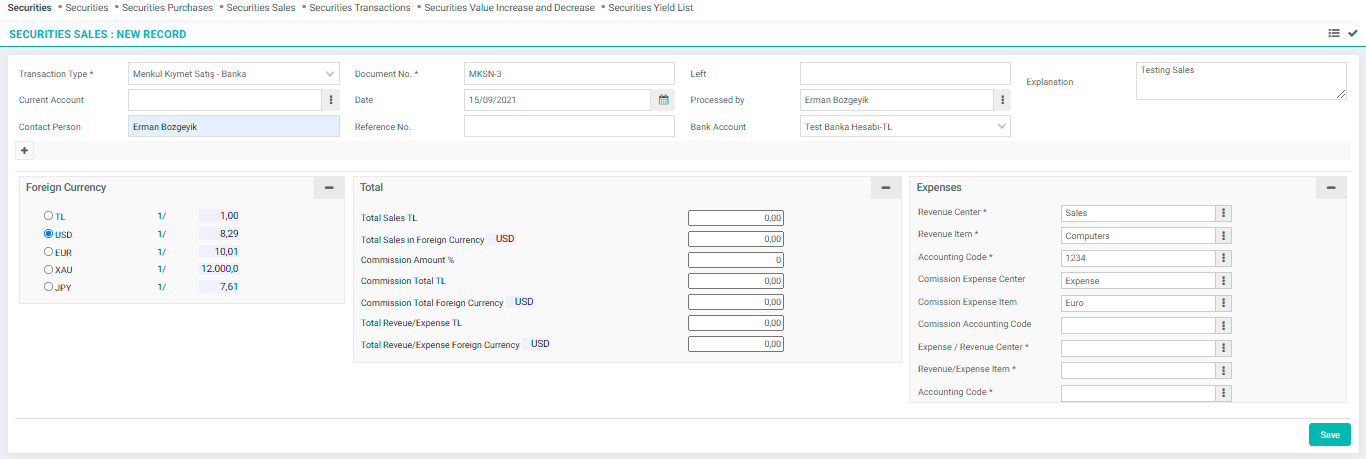

Securities Sales Transactions

The Securities Sale transaction is used to sell a security in stock. The sale can be made through a bank account or a brokerage firm. By clicking the + icon, the security to be sold is selected from the window that opens and all relevant fields are filled automatically. The Sales Value is based on the last updated value, but it can be sold by changing the price lower or higher.

Information Fields and Tables

- Transaction Type: It is the definition that determines the current, accounting, and budget transaction rules and user authorizations.

- Securities Type: It is the parametric definition that groups the securities.

- Code: Securities, especially stocks, have unique transaction codes. Workcube makes collection, grouping, and reporting according to these codes.

- Explanation: Enter the explanation and notes for the transaction.

- Nominal Value: The securities may have increased or decreased in value. The nominal value indicates one value on the book.

- Nominal Value Foreign Currency: The nominal value is written in foreign currency.

- Sales Value: Displays the unit price of this security, regardless of its face value or current market value

- Sales Value in Foreign Currency: The foreign currency equivalent of the purchase value is written.

- Quantity: The quantity sold is written.

- Total Sales: It is the diameter of the sales value and quantity.

- Total Sales in Foreign Currency: Total sales amount is written in foreign currency.

- Expense / Revenue Center: Records which budget center made the sale of securities.

- Budget Item: Records under which budget item the sale of securities will be followed.

- Securities Accounting Code: Records under which accounting account the sale of securities will be followed.

- Bank Account: Records which bank account the security was sold using. Bank transactions are made up to the purchase amount.

- Current Account: Current Account is selected when an intermediary institution is used for the sale of securities and the purchase is made by the intermediary institution. When a current account is selected, the bank cannot be used. The receivable account of the intermediary institution is run up to the purchase amount.

- Expenses: If a commission is paid to the intermediary institution, the expense center, expense item, and accounting account of the commission are selected.